First of all, a bit late but nevertheless, we wish everybody a very Happy and above all Healthy New Year with lots of Prosperity and Happiness.

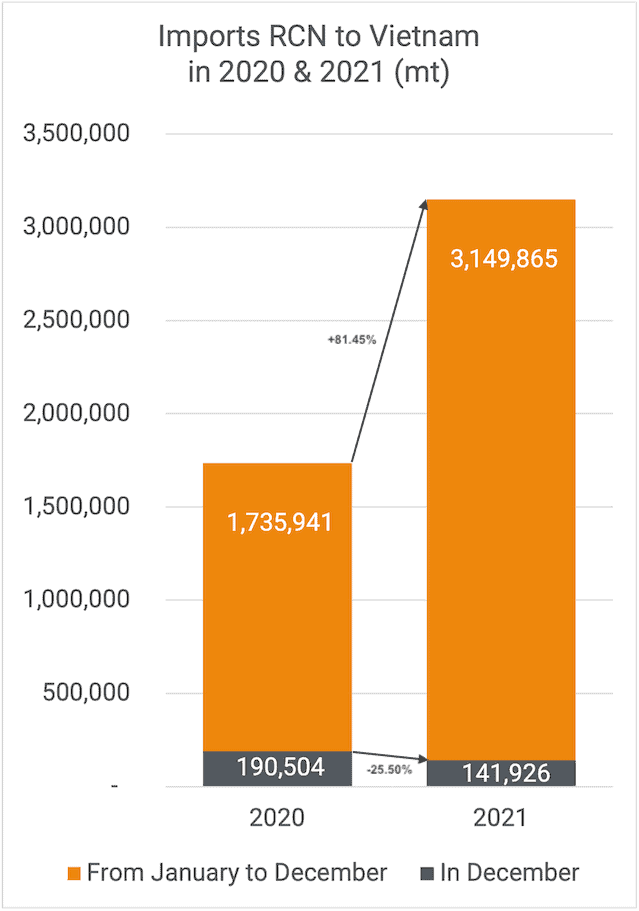

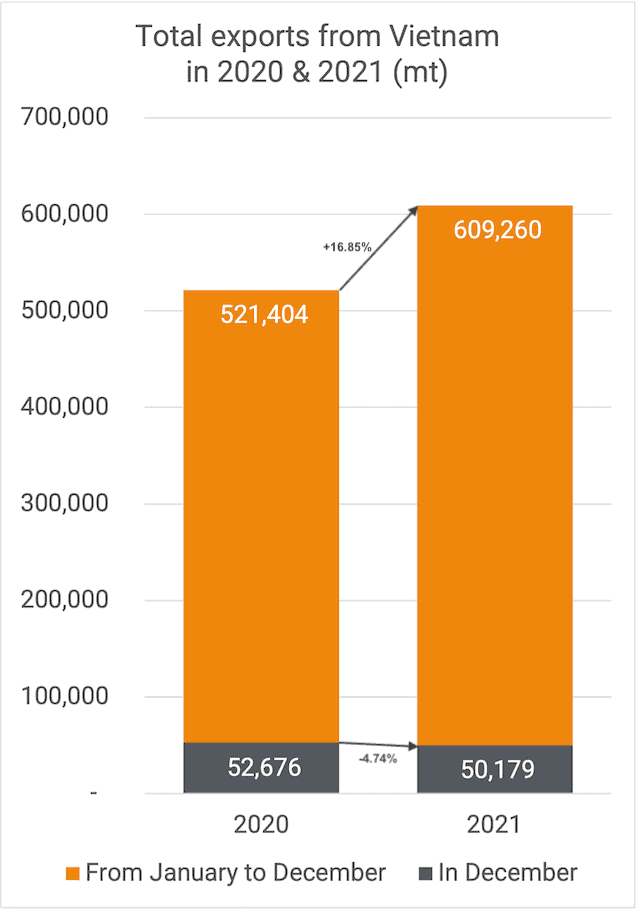

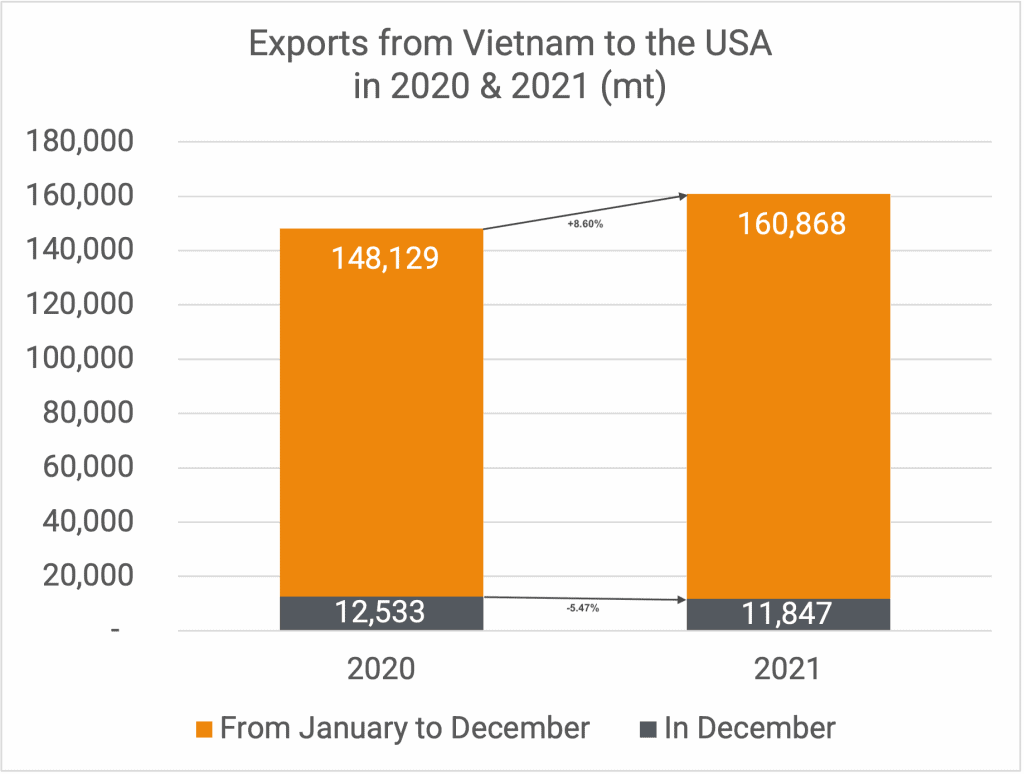

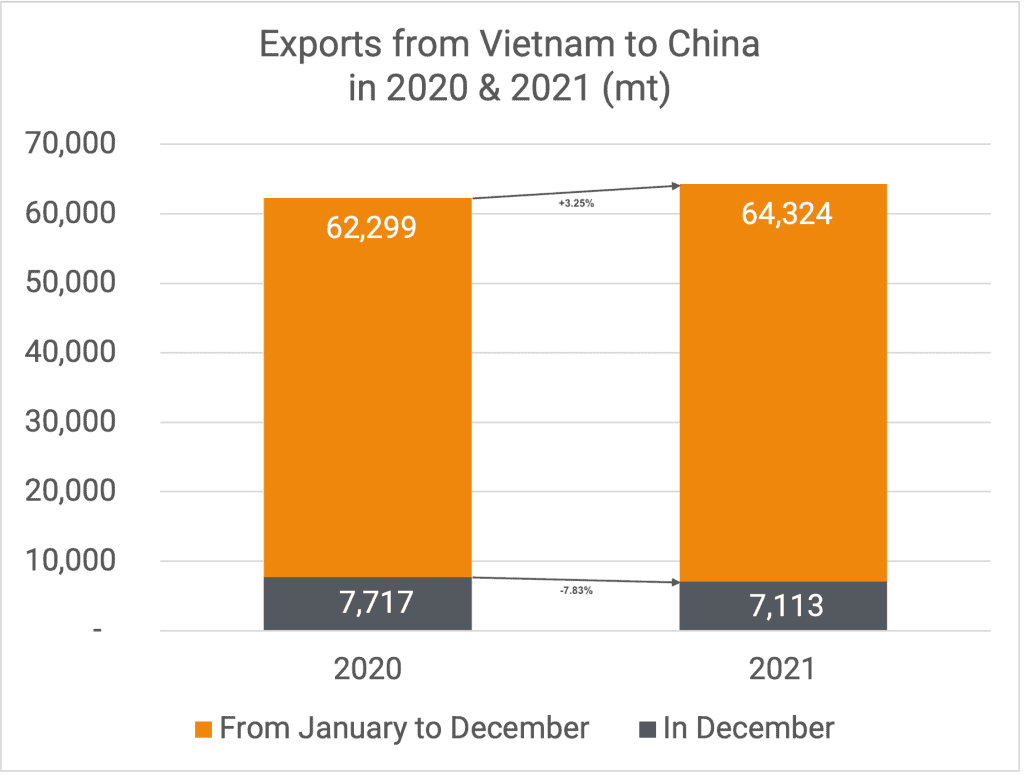

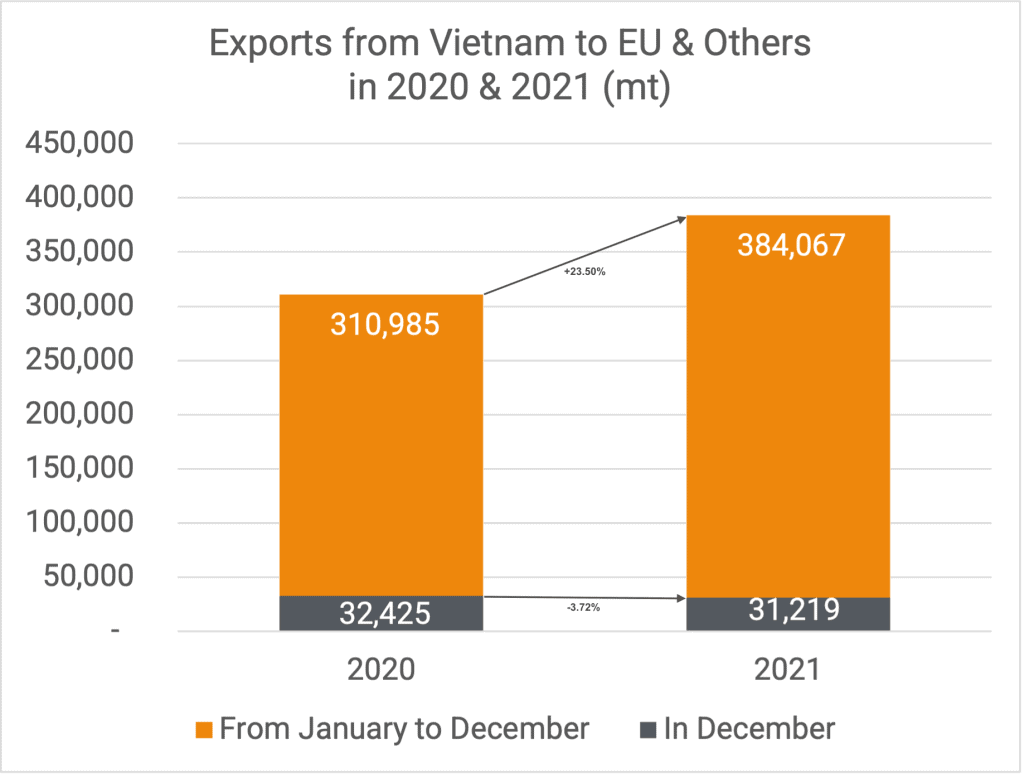

What an incredible year the Vietnamese cashew industry has had. We already talked about it last month, but we thought it would be good to break down the figures once again since we now have all figures for 2021. Importing a record 3,149,865 mt of RCN plus 88,203 mt of kernels with Testa (the equivalent of about 390,000 mt RCN) so, in fact, a total import equivalent of about 3,5 mln mt. Against that also a record number on the export of kernels, namely 609,260 mt.

If we, however, calculate with a kernel outturn of 22,5%, we see that 3,149,865 mt produces about 708,000 mt of kernels which, together with the imported kernels with Testa, makes a total availability of about 790,000 mt. In other words, there seems to be still a lot to export from Vietnam.

Demand from Europe and the USA for nearby shipments seems to have come to a standstill. This is not that unusual for the first month of the new year. However, we wonder how long this quietness will continue. Roasters seem to be well covered for the first 4-6 months of 2022. There are abundant stocks available in European and North American ports, but simultaneously we must consider what will and can happen in the next 4-6 weeks.

Because of the quietness in the market and because of the discrepancy between RCN prices and current kernel prices, many Vietnamese shippers are going to close shop earlier for TET (Chinese New Year-1st February) than they usually do. Consequently, the total quantity that will be shipped from Vietnam in the next 4-6 weeks is perceived to be a lot less than the monthly quantities shipped in the last 6 months.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.